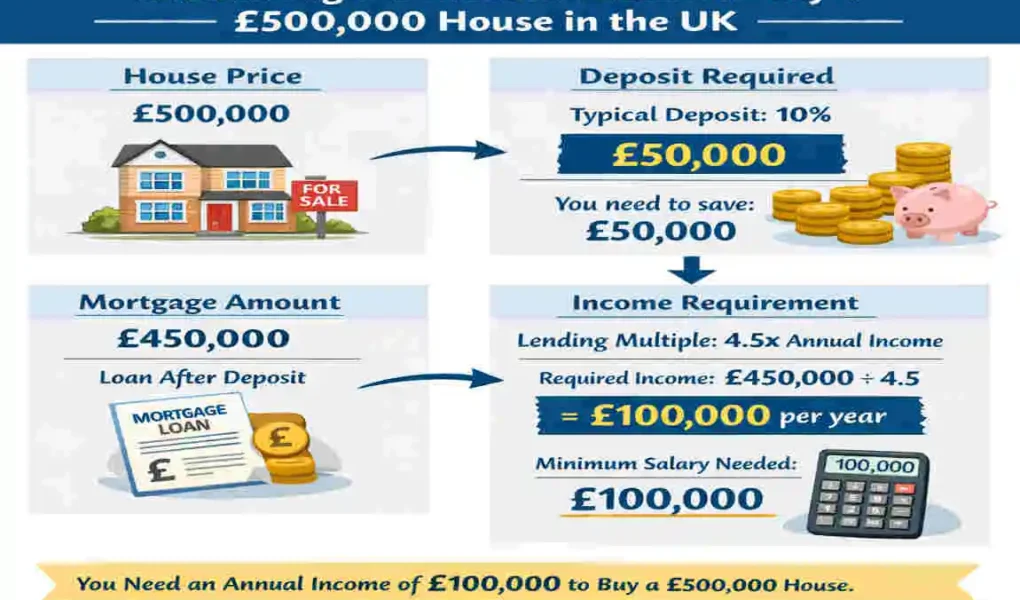

Buying a £500,000 home in the UK is a big goal, and one of the first questions people ask is: how much do I need to earn to buy a 500k house in the UK?

The simple answer is that it depends on your deposit, your income, your debts, and how lenders view your finances. Some buyers can get approved with a lower salary if they have a bigger deposit or a strong financial record. Others may need a higher income if they have existing loans or dependents.

How Mortgage Affordability Works in the UK

When you apply for a mortgage, the lender does not just look at the luxury house price. They check whether you can comfortably afford the monthly repayments.

The 4 to 4.5 Times Income Rule

A lot of UK lenders use a rule based on your annual income. In many cases, they may lend around 4-4.5 times your salary.

That means:

- If you earn £100,000, you may be able to borrow around £400,000 to £450,000

- If you earn £110,000, you may be able to borrow around £440,000 to £495,000

For a £500k mortgage calculator estimate, this is a useful starting point, but it is not the full picture. Some lenders may offer more or less depending on your situation.

Other Factors Lenders Check

Lenders also want to know if your budget can handle the loan. They usually look at:

- Credit score

- Existing debts

- Monthly spending

- Employment status

- Size of your deposit

So even if your salary looks high enough, your application can still be affected by credit card debt, car finance, or an unstable income.

How Much Do You Need to Earn for a £500K House?

The amount you need to earn depends on how much you borrow. The bigger your deposit, the smaller your mortgage needs to be.

Here is a simple guide for income required for £500k mortgage estimates:

DepositMortgage NeededEstimated Salary Needed

5% £475,000 £105,000–£120,000

10% £450,000 £100,000–£113,000

15% £425,000 £95,000–£106,000

20% £400,000 £89,000–£100,000

25% £375,000 £83,000–£94,000

This table gives a rough idea of the salary needed for a £500k house. The exact figure depends on the lender and the mortgage term.

Monthly Mortgage Payments on a £500K Home

Your income matters, but so do the monthly repayments. A longer mortgage term can lower your monthly payment, while a shorter term usually means paying more each month.

Here are rough examples of monthly mortgage payments in the UK on a £450,000 mortgage:

Example Monthly Payments

- 25-year mortgage: higher monthly payments, but less interest overall

- 30-year mortgage: lower monthly payments, but more interest over time

- 35-year mortgage: even lower monthly payments, but the total cost rises further

Interest Rate Impact

Interest rates make a huge difference. Even a small change can affect what you can afford.

- At 4%, repayments are more manageable

- At 5%, payments rise noticeably

- At 6%, affordability becomes much tighter

This is why many buyers use a mortgage income calculator UK before making an offer. It helps you see whether the numbers work for your budget.

Deposit Needed for a £500K House

Your deposit for a £500k house also affects how much you need to borrow.

Deposit %Deposit AmountMortgage Amount

5% £25,000 £475,000

10% £50,000 £450,000

15% £75,000 £425,000

20% £100,000 £400,000

25% £125,000 £375,000

A larger deposit can help you get a better deal and may reduce the income needed for approval. It can also lower your monthly repayments.

Can You Buy a £500K House as a First-Time Buyer?

Yes, it is possible, but it may be harder if you are buying alone and have a smaller deposit.

Eligibility

You may be able to buy a £500k luxury home if you use:

- First-time buyer schemes

- A joint mortgage

- Shared ownership, where available

- Family support or gifted deposit money

If you are buying with a partner, your incomes can usually be combined. That often makes it much easier to reach the level required to buy a £500k home in the UK.

Tips to Improve Mortgage Affordability

If your numbers are close, there are a few smart ways to strengthen your application.

- Increase your deposit

- Improve your credit score

- Pay off debts

- Reduce monthly spending

- Apply with a partner

- Compare mortgage lenders

- Use a mortgage broker

These steps can make a real difference, especially if you are trying to meet the lender’s affordability tests.

Common Mistakes to Avoid

Many buyers focus only on the modern house price and forget the extra costs. That can cause problems later.

Avoid these mistakes:

- Borrowing the maximum amount

- Ignoring extra buying costs

- Forgetting stamp duty

- Not budgeting for repairs

- Applying with poor credit

A good mortgage should feel manageable, not stressful.

Additional Costs Beyond the Purchase Price

When planning your budget, remember that the house price is only part of the total cost.

You may also need to pay for:

- Stamp Duty

- Solicitor fees

- Survey costs

- Mortgage arrangement fees

- Insurance

- Moving costs

- Home maintenance

These expenses can add up quickly, so always leave room in your budget.

Frequently Asked Questions

How much do I need to earn to buy a £500K house in the UK?

Usually, you may need around £83,000 to £120,000 a year, depending on your deposit and lender rules.

Can I buy a £500K house with a £50,000 deposit?

Yes, but you would still need a high income and a lender willing to offer a large mortgage.

What salary is needed for a £450,000 mortgage?

A rough estimate is around £100,000 to £113,000, depending on the lender.

How much are monthly repayments on a £500K mortgage?

It depends on the loan size, term, and interest rate. A longer term usually means lower monthly payments.

Can two people combine incomes to buy a £500K house?

Yes. Joint applications often make it easier to qualify because lenders can use both incomes.

Do all UK lenders use the 4.5× income rule?

No. Some lend less, and some may lend more based on your full financial profile.

| Factor | Details |

|---|---|

| Average House Price | £500,000 |

| Typical Deposit (10%) | £50,000 |

| Mortgage Needed | £450,000 |

| Typical Deposit (20%) | £100,000 |

| Mortgage Needed | £400,000 |

| Common Mortgage Multiplier | 4 to 4.5 × annual income |

| Estimated Income Needed (10% Deposit) | Around £100,000–£112,500 per year |

| Estimated Income Needed (20% Deposit) | Around £89,000–£100,000 per year |

| Monthly Mortgage Payment | Depends on interest rate, loan term, and deposit size |

| Other Buying Costs | Stamp Duty, solicitor fees, survey costs, mortgage arrangement fees, and moving expenses |

| Key Tip | A larger deposit reduces the mortgage amount and the income required to qualify. |